interpret kpss test result from r urca package|value of kpss test : importer I am using the KPSS test from the R urca package. My result is the following: $resProp.Dwell.3 ##### # KPSS Unit Root Test # ##### Test is of type: tau with 3 lags. palpite do jogo do bicho da vovo ceia Resultado doDeu no Poste de terça-feira dia 29/08/2023 - GigaBicho. 29 de ago. de 2023· Bem-vindo ao site GigaBicho, aqui você confere oresultado doDeu no Poste de hoje, terça-feira dia 29 de agosto, a equipedosite GigaBichoinforma osresultados doDeu no Postedo jogo do bichoao vivo..

{plog:ftitle_list}

Resultado da Blaze Cassino Brasil. Os jogos de azar estão em alta e hoje em dia é possível realizar as suas Blaze Cassino Apostas em uma variedade de jogos. Para realizar essas apostas de forma mais segura é fundamental conhecer muito bem a plataforma que você irá utilizar. 180% DE BÔNUS Até R$20,000. .

I am running a Kwiatkowski–Phillips–Schmidt–Shin test (KPSS test) in R (urca::ur.kpss). However, I am quite unsure if it is performed . I am using the KPSS test from the R urca package. My result is the following: $resProp.Dwell.3 ##### # KPSS Unit Root Test # ##### Test is of type: tau with 3 lags. We can use the kpss.test() function from the tseries package to perform a KPSS test on this time series data: library (tseries) #perform KPSS test kpss. test (data, null=" Trend ") KPSS Test for Trend Stationarity data: data .Performs the KPSS unit root test, where the Null hypothesis is stationarity. The test types specify as deterministic component either a constant "mu" or a constant with linear trend "tau".

I am running the following unit root test (Dickey-Fuller) on a time series using the ur.df() function in the urca package. The command is: summary(ur.df(d.Aus, type = "drift", 6)) KPSS test; Here, in the KPSS testing procedure, two models can be considerd : with a drift, or with a linear trend. Here, the null hypothesis is that the series is stationnary. .

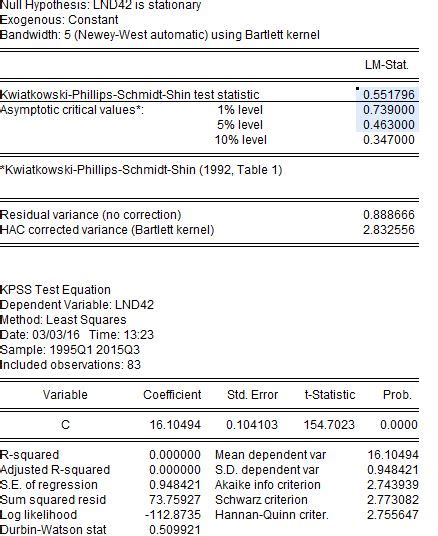

[urca:ur.ers] KPSS Test for Unit Roots: Performs the KPSS unit root test, where the Null hypothesis is stationarity. The test types specify as deterministic component either a constant .Performs the KPSS unit root test, where the Null hypothesis is stationarity. The test types specify as deterministic component either a constant "mu" or a constant with linear trend "tau".Interpretation. Value of test-statistic is 0.2241 and the Critical values for test statistics are: tau1 -2.58 -1.95 -1.62 for (1%, 5%, 10%). Thus, We reject the null, which means a unit root is present.

Representation of class ur.sp. This class contains the relevant information by applying the Schmidt and Phillips unit root test to a time series. y Object of class "vector": The time series . Here’s how to interpret the most important values in the output: Test statistic: -2.2048; P-value: 0.4943; . How to Perform a KPSS Test in R (Including Example) How to Perform a KPSS Test in Python; How to .

Kwiatkowski et al. Unit Root Test Description. Performs the KPSS unit root test, where the Null hypothesis is stationarity. The test types specify as deterministic component either a constant "mu" or a constant with linear trend "tau".. Usage Details. The function ur.df() computes the augmented Dickey-Fuller test. If type is set to "none" neither an intercept nor a trend is included in the test regression. If it is set to "drift" an intercept is added and if it is set to "trend" both an intercept and a trend is added. The critical values are taken from Hamilton (1994) and Dickey and Fuller(1981).Learn R Programming. Unit Root and Cointegration Tests for Time Series Data Description. Copy Link . install.packages('urca') Monthly Downloads. 180,241. Version. 1.3-4. License. GPL (>= 2) Maintainer. Bernhard Pfaff. Last Published. May 27th, 2024. Functions in .

We would like to show you a description here but the site won’t allow us. Prepare your time series data. Ensure that the data is stored in a vector or a time series object (e.g., ts or zoo). Use the ur.kpss() function to perform the KPSS test. This function takes the time series data as input and returns a test object containing the results of the test. Comparing results from urca with those from the tseries package seems to suggest that the p-value in urca means something different. I've read a number of similar posts but haven't found an answer to this particular question. Below is the code I'm running (the first bit runs the urca DF test, the second runs the tseries DF test). I've used zero .

Stack Overflow for Teams Where developers & technologists share private knowledge with coworkers; Advertising & Talent Reach devs & technologists worldwide about your product, service or employer brand; OverflowAI GenAI features for Teams; OverflowAPI Train & fine-tune LLMs; Labs The future of collective knowledge sharing; About the company .Performs the KPSS unit root test, where the Null hypothesis is stationarity. The test types specify as deterministic component either a constant "mu" or a constant with linear trend "tau". The KPSS Test in R. The KPSS test in R can be performed using the kpss.test() function from the tseries package. This function calculates the KPSS test statistic and compares it to the critical values to determine whether the null hypothesis should be rejected. Here is a simple way to use the kpss.test() function: # Perform the KPSS test result . We can now use the KPSS test to confirm the same: kpss_test <- kpss.test(Nile) kpss_test KPSS Test for Level Stationarity data: Nile KPSS Level = 0.96543, Truncation lag parameter = 4, p-value = 0.01. The output will display the test statistic, degrees of freedom, the p-value, and a conclusion based on the test results.

The library that I'm using is tseries and the function is kpss.test I have done a simple test using cars (a default matrix on R). . How to interpret KPSS results? Ask Question Asked 13 years, 3 months ago. Modified 7 years ago. Viewed 43k times 8 $\begingroup$ I'm using R to calculate the KPSS to check the stationarity. .

urca-class: Class 'urca'. Parent of classes in package 'urca' urca-internal: Critical values for Schmidt and Phillips Unit Root Test; ur.df: Augmented-Dickey-Fuller Unit Root Test; ur.df-class: Representation of class ur.df; ur.ers: Elliott, Rothenberg and Stock Unit Root Test; ur.ers-class: Representation of class ur.ersWe would like to show you a description here but the site won’t allow us.

Unit Root Tests from Berhard Pfaff's "urca" Package: Elliott-Rothenberg-Stock Test for Unit Roots: To improve the power of the unit root test, Elliot, Rothenberg and Stock proposed a local to unity detrending of the time series. . [urca:ur.ers] KPSS Test for Unit Roots: . additional test results to be printed. Note. This video is on how to conduct unit root tests in R software. You need to install "urca" package. summary-methods: Methods for Function summary in Package 'urca' sumurca-class: Representation of class sumurca; UKconinc: Data set for the United Kingdom; UKconsumption: Data set for the United Kingdom; UKpppuip: Data set for the United Kingdom: ppp and uip; urca-class: Class 'urca'. Parent of classes in package 'urca'

value of kpss test

Interpreting the Results. The KPSS test authors derived one-sided LM statistics for the test. If the LM statistic is greater than the critical value (given in the table below for alpha levels of 10%, 5% and 1%), then the null hypothesis is rejected; the series is non-stationary. This week, in the MAT8181 Time Series course, we’ve discussed unit root tests. According to Wold’s theorem, if is (weakly) stationnary then where is the innovation process, and where is some deterministic series (just to get a result as general as possible). Observe that as discussed in a previous post. To go one step further, there is also the Beveridge-Nelson .We would like to show you a description here but the site won’t allow us.

I preformed a KPSS test in R using kpss.test from package tseries and these are the results: KPSS Level = 1.966, Truncation lag parameter = 5, p-value = 0.01 Warning message: In kpss.test(coke[,5], null = "Level") : p-value smaller than printed p-value Will anyone that is more knowledgeable about the subject please help me interpret this?

I am a bit confused about the three different Augmented Dickey–Fuller tests (none,drift, trend). Based on the Wikipedia page on the topic, those three ADF tests are almost the same in that the unit root test is carried out under the null hypothesis r = 0 against the alternative hypothesis of r < 0 and DF = r/SE(r).. Is the only difference the critical value?Performs the Augmented Dickey-Fuller test for the null hypothesis of a unit root of a univarate time series x (equivalently, x is a non-stationary time series). Rdocumentation. powered by. Learn R Programming. aTSA (version 3.1.2.1) Description. Usage Value, , .This is most likely because the ca.jo R function in the urca package requires our lag order to be two or . The only difference is that the implementations of the Johansen test are different between R's urca and MatLab's . In addition we should be extremely cautious of interpreting these results as I have only used one years worth of data .A matrix for test results with three columns (lag,Z_rho or Z_tau, p.value) and three rows (type1, type2, type3). Each row is the test results (including lag parameter, test statistic and p.value) for each type of linear equation. Note. Missing values are removed. Author(s) Debin Qiu References. Phillips, P. C. B.; Perron, P. (1988).

I'm having a problem with the Dickey-Fuller p-values and test statistic for unit root test in R. I tried using functions: urca::ur.df() fUnitRoots::adfTest() tseries::adf.test() All of them showed different results for the same test settings (lag, .This function uses the package 'urca' to perform unit root tests on a pre-defined time series. Unlike urca functions, it returns a meaningful table summarizing the results. . (not for KPSS), '2.5pct', '5pct' or '10pct' Value. A list object. The first element is a data.frame with the test statistics, the critical values and the test results .

nail polish remover paint test

nyc lead paint test

Resultado da Crown Slots. O aplicativo oficial é mais emocionante e suave. Instale agora e ganhe R$ 10. BAIXE. 59%. O jogo está carregando, seja paciente. Ele demorará um pouco mais para abrir pela primeira vez.

interpret kpss test result from r urca package|value of kpss test